Agro finance often shows up when things go wrong. A flood hits. A drought burns the crops. A pest outbreak wipes out a season’s hard work. Then money moves. Insurance claims are filed. Governments announce relief. Banks restructure loans. But by then, the damage is already done.

Is compensation enough to protect farmers? Not really. It helps them survive the loss, but it rarely protects them from experiencing it in the first place. Survival and stability are not the same thing.

Prevention shifts the focus. Instead of asking how to repay losses, it asks how to reduce risk before planting even begins. That mindset changes everything in agro finance.

Compensation in Agro Finance: What Does It Really Mean?

Compensation in agro finance means financial support after a loss has already occurred. The system responds once crops fail, yields drop, or income collapses.

First, there are crop insurance payouts. A farmer pays a premium. If the expected revenue is $10,000 but due to drought, the actual revenue falls to $4,000, the insurer may cover part of the $6,000 loss. But payouts often take time. Assessments must be verified. Claims must be processed. Meanwhile, the farmer still has bills to pay.

Second, government relief funds. After disasters, authorities may announce grants or subsidies. Suppose a region loses $1 million in crop value. Relief may cover only a fraction, say 30–40%. That means many farmers still absorb significant losses themselves.

Third, loan restructuring. Banks may extend repayment terms or reduce interest temporarily. For example, a $5,000 loan due in one year may be stretched to three years. The pressure eases, but the debt remains. In some cases, total interest paid even increases over time.

Compensation feels helpful because it provides immediate emotional relief. It signals support. But it comes late when the crop is already gone. The income gap has already hit. It fixes part of the financial damage, yet it cannot restore lost time, lost productivity, or lost opportunity.

What Does Prevention Look Like in Agro Finance?

Prevention in agro finance is about acting before the loss happens. Instead of asking, “How do we recover?” it asks, “How do we reduce risk from day one?” That shift alone makes prevention stronger than compensation.

Weather intelligence before planting is a powerful example. If data shows a high probability of drought in a specific region, farmers can shift crop choices or adjust planting schedules. Imagine expected revenue is $12,000 from a water-intensive crop. But drought risk suggests yield could fall by 40%. Switching early to a drought-resistant crop that generates $9,000 may seem smaller, but it protects income stability. That is prevention in action.

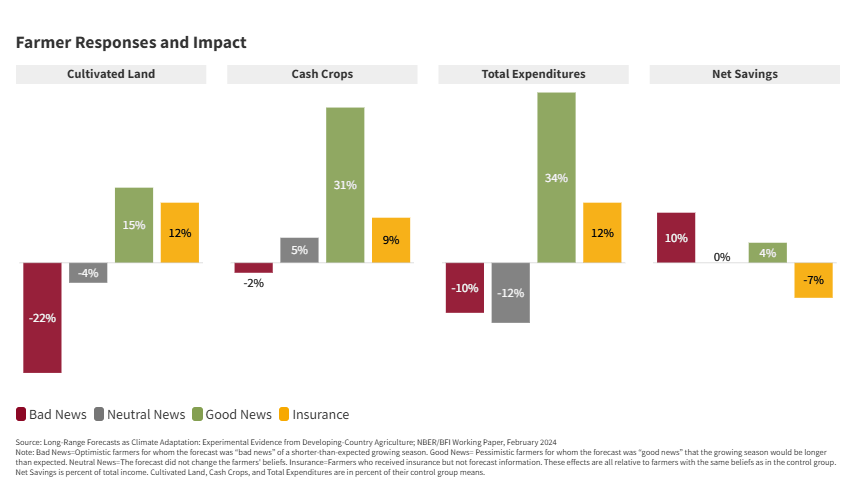

Research at the University of Chicago says that better weather forecasts help farmers adapt to climate change and guess it more accurately.

Image source: Better Weather Forecasts Can Help Farmers Adapt to Climate Change

Smart credit scoring based on real farm data also changes the game. Traditional lending often relies on past repayment history alone. Preventive models use soil data, weather patterns, crop cycles, and market prices. If risk indicators show a 30% probability of yield drop, lenders can adjust loan size or repayment timing before disbursing funds. That reduces defaults instead of reacting to them later.

Why Prevention in Agriculture is Better Than Compensation?

Prevention in agro finance is often more effective than compensation because it reduces risks before financial losses occur. AI-powered monitoring, weather forecasting, crop disease detection, and smart irrigation systems can help farmers protect crops early rather than depending on post-disaster financial aid. Preventive strategies also reduce insurance costs, improve productivity, and support long-term agricultural sustainability. According to research published by the Food and Agriculture Organization (FAO), early risk management systems can significantly reduce crop losses caused by climate and environmental challenges. Similarly, studies from The World Bank highlight that proactive agricultural financing improves resilience and financial stability for small-scale farmers. Adding AI-based prevention tools may help governments and financial institutions reduce compensation burdens over time.

The Role of Technology in Prevention in Agro Finance

Technology is what makes prevention practical. Without data and digital systems, prevention remains a theory. With technology, it becomes measurable and scalable.

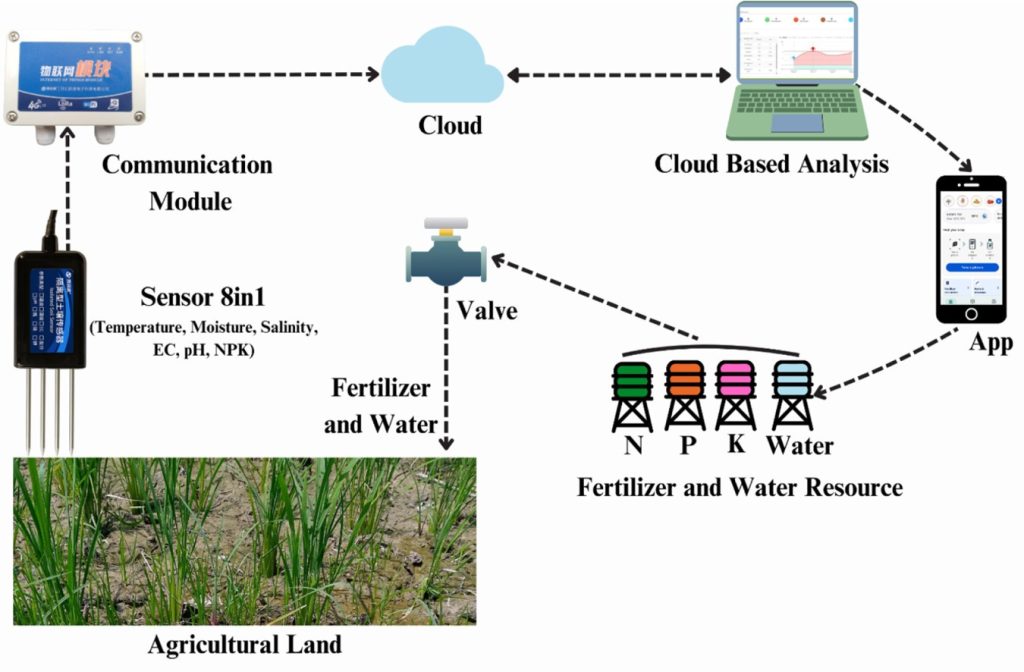

Data collection is the foundation. Satellite imagery, IoT sensors, and field-level reporting provide real-time visibility into soil health, rainfall patterns, crop growth, and pest movement. Instead of waiting for yield reports at the end of the season, lenders and farmers can see risk forming in real time. That alone reduces uncertainty.

Image: collected from IoT-driven smart agricultural technology for real-time soil and crop optimization

Artificial intelligence takes it further. AI models analyze historical weather, soil data, and market trends to predict potential yield outcomes. If data shows a 35% probability of production loss in a region, financial institutions can adjust loan terms early. Smaller, smarter loans reduce default risk before it happens.

Digital credit scoring also improves decision-making. Instead of relying only on past repayment records, fintech platforms use farm productivity data and climate risk indicators. This creates dynamic risk profiles. The result is better loan pricing, better timing, and fewer surprises.

Technology also powers early warning systems. Flood alerts, pest detection algorithms, and drought forecasting tools can send automated notifications to farmers. Acting two weeks earlier can mean saving thousands in crop value. That is the financial impact of predictive systems.

Get Smarter Agricultural Insights With Soluta

Monitor weather, reduce risks, improve farm decisions, and stay ahead with AI-driven agricultural intelligence.

Download the App3 Case Studies of Prevention in Agri Finance

1. ICICI Lombard & Weather-Based Crop Insurance (India)

In India, weather-indexed insurance shifted the model from traditional compensation to predictive triggers. Instead of waiting for physical crop assessment, payouts were triggered by rainfall data collected from weather stations.

According to reporting from The Economic Times, weather-based insurance reduced claim settlement time significantly compared to traditional crop-loss verification systems. In many regions, payouts were processed within weeks because rainfall deviation data automatically activated claims.

Mathematically, this reduced administrative lag and moral hazard. If rainfall dropped 50% below the historical average during a critical growth phase, payouts were triggered immediately. Farmers did not need to prove field-level damage. The system prevented liquidity collapse during the season, not months later.

The result? Faster support, lower processing cost, and more predictable risk modeling for insurers.

2. The Climate Corporation (United States)

In the U.S., preventive agro finance has been strengthened through predictive analytics. The Climate Corporation, owned by Bayer, provides field-level weather forecasting and risk modeling tools.

According to coverage in The Wall Street Journal, farmers using data-driven planting insights improved yield predictability by aligning planting decisions with soil moisture and weather forecasts.

For example, if predictive models showed a high probability of delayed rainfall, planting schedules were adjusted. Instead of facing a 20–30% yield drop due to early dry spells, farmers optimized timing and reduced exposure.

This is prevention. It does not wait for a payout. It reduces the probability of loss before the loan cycle matures.

3. Pula Advisors (Africa & Asia)

Pula Advisors works across Africa and Asia integrating insurance with digital advisory tools. Pula has insured millions of smallholder farmers using satellite data and automated risk monitoring.

Instead of traditional field inspections, satellite vegetation indices detect crop stress early. If abnormal stress patterns are identified, interventions are triggered before full crop failure.

In Kenya, index-based insurance programs supported by digital monitoring reduced claim fraud and cut operational costs. This allowed insurers to lower premium pricing while increasing coverage scale.

From a financial standpoint, when operational cost drops by even 10–15%, premium affordability improves. That expands coverage and reduces systemic risk in rural lending markets.

Final Words

Agro finance cannot stay reactive in a world of rising climate risk and market volatility. Compensation has its place, but it should be the safety net, not the strategy. Prevention, powered by data and intelligent systems, strengthens farmers before losses occur.

It protects cash flow, credit health, and long-term growth. From an expert standpoint, the future belongs to predictive finance. And when we protect farmers early, we protect the entire food economy.